Building the digital future for financial instruments

Release date: 27 Jan 2022

As an international exchange organization and innovative market infrastructure provider, Deutsche Börse is paving the way for regulatory compliant, fully digital post-trade transformation. In a guest article for Securities Finance Monitor, Gerd Hartung, head of Digital Markets and Thomas Wissbach, senior vice president in New Digital Markets, discuss the milestones reached and road ahead for the D7 platform as part of this evolution.

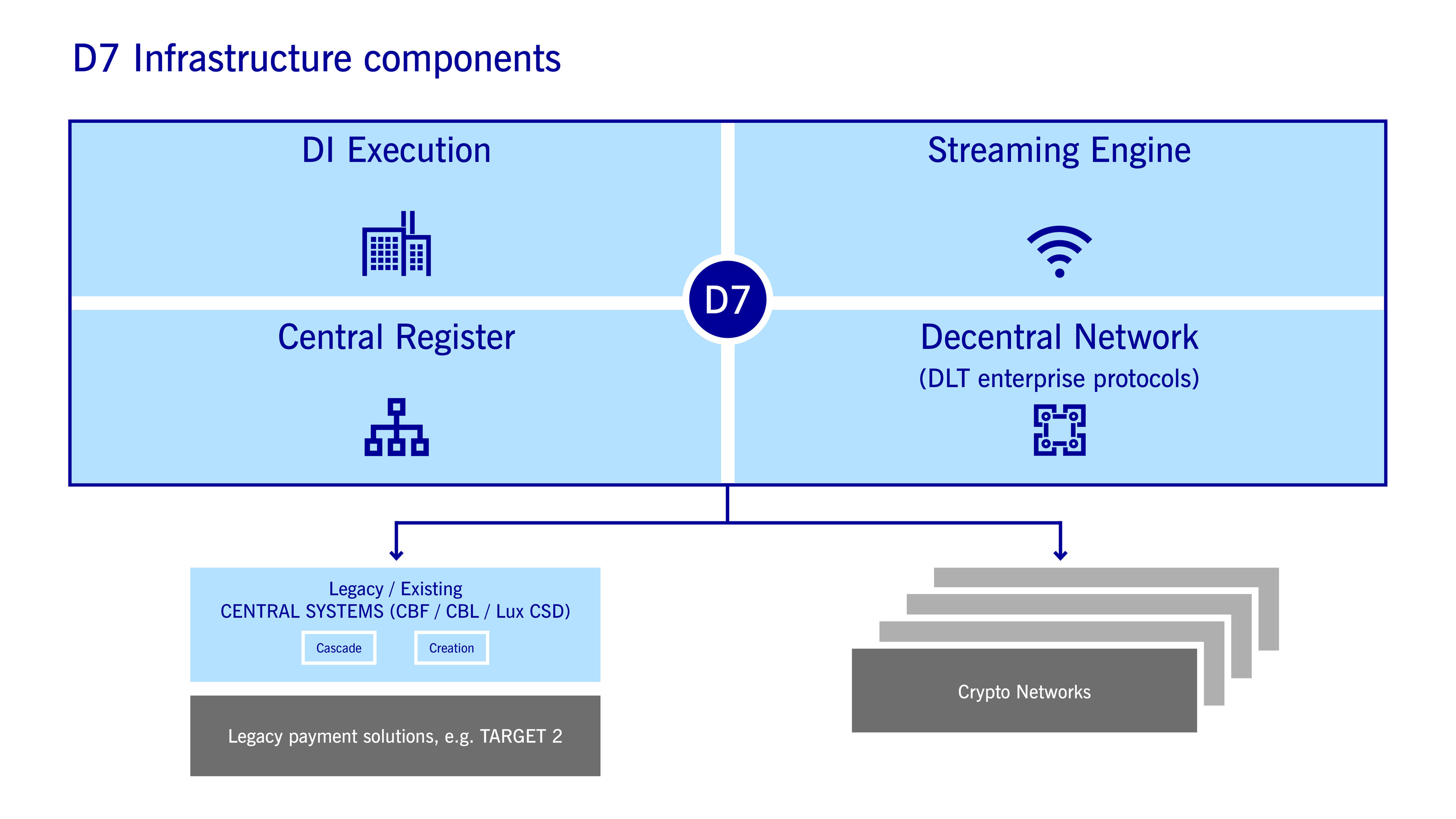

D7 is the new infrastructure component of Deutsche Börse’s “7 Market Technology” series

D7 is the new infrastructure component of Deutsche Börse’s “7 Market Technology” series

The D7 platform is the new infrastructure component of Deutsche Börse’s “7 Market Technology” series, which covers trading, clearing, settlement and analytics across global networks and various asset classes. Financial institutions will be able to issue, register and process electronic financial instruments on the new platform, which enables the end-to-end processing of the entire life cycle of digital assets.

The digitization of processes has been a major focus across the financial industry, but one of the core ideas underpinning D7’s development is on the financial instruments themselves. The aim is to create a standard digital description for financial instruments so that there are common, in-sync representations, similar to the music industry using an MP3 format for tracks.

These standard representations will flow through existing regulated environments, such as central securities depositories (CSDs), as well as new environments such as decentralized networks. The digital instrument is the “back bone” which will be used in both worlds, explained Hartung.

In June 2021, Germany’s Electronic Securities Act (eWpG) entered into force, establishing a legal basis for the admission of rights through electronic securities registers, known as a central registry, and adding a new license category for maintaining a crypto securities register.

This law provides much needed certainty for the handling of digitized instruments via traditional structures such as CSDs in the case of the central registry, while crypto registers outline how securities can be managed in the future on a decentralized network, for which there is no need for CSD registration of instruments.

From a technology perspective, these are two parallel worlds that need to be interoperable for issued digital instruments to be able to move between them. From a product perspective, it’s another way of issuing securities in a more convenient way, and how that translates to adoption and products is driven by market participants, said Wissbach.

Market and tech partners

Deutsche Börse’s D7 partners include both market participants and technology solution providers. The financial technology firm Digital Asset is helping to build out the standard representation of digital instruments, while blockchain enterprise software provider R3 and cloud computing and virtualization technology company VMWare are working on the protocols for decentralized networks. The team is also tapping Microsoft for cloud components.

On the market side, there are over a dozen issuers and agents actively involved in building the model, as well as large buy-side institutions joining working groups to understand the process end-to-end.

“We need to understand the complete flow from the issuer, through the whole ecosystem, onto the investor and back,” said Hartung. “And that is why we are having not only issuers and banks around the table, but also end investors.”

Some of the global and German financial institutions signed on include BNP Paribas, Citi, DekaBank, Deutsche Bank, dwpbank, DZ Bank, Goldman Sachs, Raiffeisen Bank International and Vontobel.

Adoption hurdles

The vision for D7 is to be a “major connector” not only for inhouse developments, but also for the proliferation of independent blockchain and DLT-based services, said Wissbach, adding that take-up tends to be spurred by early adopters that push the technology and service options.

One example of an emerging company that can connect to D7 is HQLAᵡ, a platform that enables market participants to transfer ownership of baskets of securities across disparate collateral pools with atomic settlement, and there are also calls to extend this collateral basket lending service to repo transactions.

Participants of DLT-based services will need to become familiar with the operation of network nodes, which are responsible for the accuracy and reliability of storing the entered data in the distributed ledger and have components such as computing resources, ledger, wallet and keys, and protocol applications.

In theory, it’s understood that participants should be more independent running their own nodes on networks, which will provide them more end-to-end flexibility. In practice however, it is not an easy exercise to integrate these network nodes into the existing legacy infrastructure, which requires resources, budgets, business case justification, as well as liability considerations as a node operator.

“We are all conscious that a network, in total, can only be as strong as the weakest node in the network,” said Hartung. “Everyone who operates a node needs to fulfil certain criteria, needs to accept due diligence. And that has a consequence in terms of the service levels that need to be provided and also liabilities that need to be entered into, as well as alignment with the respective regulators.”

Decentralized payments

The biggest unanswered industry-wide question is: how are payments going to be organized on decentralized networks? There is no “ultimate solution” so far, explained Wissbach. Bitcoin is not acceptable for institutional clients, there are warning flags over stablecoins and their reserves, and a central bank digital currency (CBDC), such as a “digital euro” seems to be far away.

This has prompted Deutsche Börse to consider falling back on a “trigger” solution, which was successfully tested in early March 2021 along with Germany’s central bank and Finance Agency. It comprises a DvP settlement interface that connects with electronic securities on distributed ledger technology (DLT) and a “trigger chain” linked with TARGET2, the Eurosystem’s large-value payment system. What’s important is that this technological bridge between blockchain and traditional payment systems does not need a CBDC.

From the exchange’s perspective, there are no limitations for any and all of the possibilities to achieve a payment on a distributed network, except in terms of what is acceptable to clients and regulators while also being available for use.

“We are not limited to one of those solutions, we could connect to multiple ones, and this is related to where our clients have their liquidity pools. Definitely, a central bank digital currency solution is what we would go for but as long as we don’t have it, we need to look what’s available and we need to use those,” said Wissbach.

Development timeline

Aside from Germany’s eWpG laws, other jurisdictions have or are expecting to pass legislation: Luxembourg’s blockchain act is also applicable for crypto registers, for example. Where there’s likely to be a lot of attention, however, is on the European Union-wide level. A much-anticipated pilot regime for market infrastructures based on DLT is expected to be implemented in early 2023.

The EU Commission proposal is part of a “Digital Finance” package that seeks to boost the potential of innovation and competition while mitigating associated risks, as well as provide legal clarity for crypto asset markets. Permissions granted under the resulting regulation would allow market participants to operate a DLT market infrastructure and to provide their services across all EU member states.

In December 2021, Deutsche Börse established a new central register at the German Central Securities Depository Clearstream, forming the basis for issuance and custody of dematerialized securities compliant with eWpG for the first time in Germany, and linked to TARGET2-Securities, the pan-European securities settlement engine.

In June 2022, Deutsche Börse is expecting to launch the digital instrument including the option to issue into the central register at the CSD next to traditional paper-based rails. It’s expected that over 80% of German securities will be eligible to be digitized as of mid-June 2022, enabling same-day-issuance and paperless, automated straight-through processing. By the end of the year, there’s a plan for a decentralized network solution that will incorporate crypto assets, with further products to be enabled over the course of 2023.

A lot depends on sufficient market support and how the broader ecosystem adapts to these opportunities, Hartung noted: “We expect a fully regulated crypto space to develop that operates within the financial industry. It is existing, it further progresses, and we expect at this stage it is here to stay.”

About the Experts

Gerd Hartung Senior Vice President, Head of New Digital Markets Deutsche Börse Group

Gerd Hartung Senior Vice President, Head of New Digital Markets Deutsche Börse Group

Gerd Hartung is Head of New Digital Markets at Deutsche Börse, a team exploring the opportunities within the framework of blockchain and distributed ledger technology. He has been with Deutsche Börse since 1996, working in a variety of different roles. In a joint project with Deutsche Bundesbank, he developed a comprehensive Collateral Management Service for the German market, which became the backbone of Deutsche Börse’s Euro GC Pooling segment. After Clearstream’s merger with Cedel in 2000, he managed a cross-location team in Frankfurt, Luxembourg and London and was responsible for the Product Management of all Collateral Management Services. In 2004, Gerd was appointed Director and Head of the Market and Business Development at Clearstream. Prior to joining Deutsche Börse Group, Gerd was a Project Manager at Deutsche Bank, where he developed IT solutions for Risk Controlling as well as for Asset /Liability Management. He graduated in Mathematics with Macroeconomics as a second subject and in addition, he holds a PhD in Mathematics – both from the Technical University of Darmstadt (Germany).

Thomas Wissbach Senior Vice President New Digital Markets Deutsche Börse Group

Thomas Wissbach Senior Vice President New Digital Markets Deutsche Börse Group

Thomas Wissbach is Senior Vice President in New Digital Markets. Previously, he was heading the product design team for Eurex Clearing’s collateral services. During his multiple years’ career in the area of clearing and settlement for securities and derivatives, he covered various roles in the industry. Before joining Deutsche Börse Group, he was Head of Product Management for Domestic Custody Services at Deutsche Bank. During his time at Dresdner Bank, he was heading the Product Development team for Domestic Custody Services and prior to that the Operations team for Exchange Traded Derivatives. He served many years as chairperson to key market committees in Europe covering the introduction and development of clearing services for both, derivatives and cash (securities) market products.

This article was first published on Finadium.com on 27 January 2022.

Welcome to the Deutsche Börse Group! If you give us your consent and click on "Accept All", we use cookies and related technologies on our website to give you the best possible online experience. You also have the option of only giving your consent for certain categories. Please note that based on your settings, not all functions of the website may be available. Further information and how you can withdraw your consent can be found in ourPrivacy Notices

Show detailsHide details

Save & Close

Accept all

Decline all

Cookie Definition

Über Cookies

Strictly necessary

Performance

Targeting

Strictly necessary cookies allow core website functionality such as user login and account management. The website cannot be used properly without strictly necessary cookies.

Cookie report

Name

Provider / Domain

Gültig bis

Beschreibung

ApplicationGatewayAffinityCORS

www.deutsche-boerse.com

Session

This cookie is used by the Application Gateway in addition to ApplicationGatewayAffinity to maintain sticky session even on cross-origin requests.

ApplicationGatewayAffinity

www.deutsche-boerse.com

Session

This cookie is used by the Application Gateway to maintain sticky session.

ApplicationGatewayAffinityCORS

deutsche-boerse.com

Session

This cookie is used by the Application Gateway in addition to ApplicationGatewayAffinity to maintain sticky session even on cross-origin requests.

CookieScriptConsent_new

.deutsche-boerse.com

1 year

This cookie is used by Cookie-Script.com service to remember visitor cookie consent preferences. It is necessary for Cookie-Script.com cookie banner to work properly.

For continued stickiness support with CORS use cases after the Chromium update, we are creating additional stickiness cookies for each of these duration-based stickiness features named AWSALBCORS (ALB).

ApplicationGatewayAffinity

deutsche-boerse.com

Session

This cookie is used by the Application Gateway to maintain sticky session.

Performance cookies are used to see how visitors use the website, eg. analytics cookies. Those cookies cannot be used to directly identify a certain visitor.

Cookie report

Name

Provider / Domain

Gültig bis

Beschreibung

_pk_ses.8.b399

deutsche-boerse.com

30 minutes

This cookie name is associated with the Piwik open source web analytics platform. It is used to help website owners track visitor behaviour and measure site performance. It is a pattern type cookie, where the prefix _pk_ses is followed by a short series of numbers and letters, which is believed to be a reference code for the domain setting the cookie.

_pk_ses.8.5ea9

www.deutsche-boerse.com

30 minutes

This cookie name is associated with the Piwik open source web analytics platform. It is used to help website owners track visitor behaviour and measure site performance. It is a pattern type cookie, where the prefix _pk_ses is followed by a short series of numbers and letters, which is believed to be a reference code for the domain setting the cookie.

_pk_id.8.b399

deutsche-boerse.com

1 year

This cookie name is associated with the Piwik open source web analytics platform. It is used to help website owners track visitor behaviour and measure site performance. It is a pattern type cookie, where the prefix _pk_id is followed by a short series of numbers and letters, which is believed to be a reference code for the domain setting the cookie.

_pk_id.8.5ea9

www.deutsche-boerse.com

1 year

This cookie name is associated with the Piwik open source web analytics platform. It is used to help website owners track visitor behaviour and measure site performance. It is a pattern type cookie, where the prefix _pk_id is followed by a short series of numbers and letters, which is believed to be a reference code for the domain setting the cookie.

Targeting cookies are used to identify visitors between different websites, eg. content partners, banner networks. Those cookies may be used by companies to build a profile of visitor interests or show relevant ads on other websites.

This cookie is set by Youtube to keep track of user preferences for Youtube videos embedded in sites;it can also determine whether the website visitor is using the new or old version of the Youtube interface.

__Secure-ROLLOUT_TOKEN

.youtube.com

6 months

It is used to authenticate and authorize users, ensuring that only legitimate requests are processed.

This cookie is used to store the user's consent and privacy choices for their interaction with the site. It records data on the visitor's consent regarding various privacy policies and settings, ensuring that their preferences are honored in future sessions.

Ein Cookie ist eine kleine Textdatei, die ein Webportal auf Ihrem Rechner, Tablet-Computer oder Smartphone hinterlässt, wenn Sie es besuchen. So kann sich das Portal bestimmte Eingaben und Einstellungen (z. B. Login, Sprache, Schriftgröße und andere Anzeigepräferenzen) über einen bestimmten Zeitraum „merken“, und Sie brauchen diese nicht bei jedem weiteren Besuch und beim Navigieren im Portal erneut vorzunehmen.